Introduction: The Hidden Cost That Never Goes Away

In Part 1, we discussed how load mutual funds charge sales commissions that immediately reduce your invested capital. But the real damage caused by load funds often goes far beyond the upfront fee.

In this second part, we’ll look deeper into why load mutual funds continue to work against investors over time, how they distort decision-making, and why avoiding them can significantly improve long-term investment outcomes.

Load Funds Create an Unnecessary Performance Handicap

Every investment begins with a starting line. Load mutual funds start investors behind that line.

When you pay a sales load:

- Your money needs to recover the fee before earning real returns

- The fund must outperform simply to break even

- Market volatility makes recovery harder

No-load funds don’t have this handicap. They let compounding work immediately.

Sales Incentives Distort Advice

One of the biggest problems with load mutual funds is how they are sold.

Load funds exist primarily to:

- Pay commissions

- Reward distribution networks

- Incentivize sales, not performance

This structure creates a conflict of interest where recommendations may be influenced by:

- Higher commissions

- Sales quotas

- Product incentives

Good investing should be driven by strategy—not sales pressure.

Breakpoints Are Not the Advantage They Appear to Be

Supporters of load funds often mention “breakpoints,” which reduce commission percentages for larger investments.

The reality:

- Breakpoints still involve paying fees

- Investors must invest more capital to reduce losses

- Many investors never qualify or are not informed properly

Avoiding the fee entirely is almost always better than paying a reduced one.

Opportunity Cost Is Often Ignored

Money paid in commissions is money that:

- Can’t compound

- Can’t be reinvested

- Can’t earn returns

Even small loads create significant opportunity costs over time.

A 5% load paid today could represent:

- Tens of thousands of dollars lost over decades

- Reduced retirement income

- Slower portfolio growth

These losses are silent—but permanent.

Load Funds Encourage Inertia

Because selling load funds may trigger:

- Back-end loads

- Deferred sales charges

- Regret over sunk costs

Investors may:

- Hold underperforming funds too long

- Delay portfolio improvements

- Avoid rebalancing

This emotional friction harms long-term performance.

The Myth of Superior Management

Load funds are often marketed as “professionally managed” or “actively supervised.”

However:

- No evidence consistently shows load funds outperform no-load funds after fees

- High turnover increases tax inefficiency

- Active management does not justify commissions

Quality management exists across both categories—but cost still matters.

Tax Inefficiency Adds Another Layer of Cost

Many load funds are actively traded, which can result in:

- Higher capital gains distributions

- Unexpected tax bills

- Reduced after-tax returns

No-load index and low-turnover funds are often:

- More tax-efficient

- More predictable

- Easier to manage in taxable accounts

Taxes are another hidden cost that compounds negatively.

Complexity Benefits the Seller, Not the Investor

Load mutual funds often come with:

- Multiple share classes

- Confusing fee structures

- Hard-to-compare disclosures

Complexity makes it easier to:

- Hide true costs

- Discourage comparison

- Create dependence on advisors

Simple, transparent investments favor the investor.

Technology Has Made Load Funds Obsolete

Today, investors can:

- Buy funds directly online

- Access professional-grade research

- Build diversified portfolios cheaply

There is no longer a need to pay commissions for access.

The market has evolved—but load funds remain stuck in the past.

Behavioral Damage: Paying More Feels Like Commitment

Some investors believe paying a commission makes them:

- More committed

- Less likely to panic sell

In reality:

- Discipline comes from strategy, not fees

- High costs don’t prevent emotional mistakes

- Education and planning matter more

Paying more does not equal investing better.

Better Alternatives Exist

Instead of load mutual funds, investors can choose:

- No-load mutual funds

- Index funds

- ETFs with low expense ratios

These options offer:

- Lower costs

- Greater flexibility

- Transparent pricing

- Strong long-term performance potential

Modern investing favors efficiency.

When Load Funds Might Be Defended (Rarely)

In limited cases, load funds may be considered if:

- An advisor provides ongoing, holistic financial planning

- Fees are clearly disclosed

- Value received exceeds cost

Even then, total cost should be scrutinized carefully.

Long-Term Impact on Retirement Planning

Over decades, load funds can:

- Reduce retirement balances

- Increase required contributions

- Delay financial independence

Avoiding unnecessary fees is one of the easiest ways to improve retirement outcomes—without increasing risk.

Final Thoughts: Compounding Works Best Without Friction

The most powerful force in investing is compounding. Load mutual funds place friction in front of that force.

By avoiding load funds, investors:

- Start with more capital

- Keep more of their returns

- Maintain flexibility

- Reduce conflicts of interest

You don’t need to beat the market to succeed—you need to stop paying against yourself.

Choosing no-load, low-cost investments is not about being cheap.

It’s about being smart, intentional, and long-term focused.

Word Count:

760

Summary:

Five more reasons why you should select no load mutual funds rather than load funds. Pick a load mutual fund and you could lose a significant amount of your investment profit.

Keywords:

no load mutual funds, mutual funds, load funds, no load funds, no-load funds

Article Body:

Copyright 2006 Michael Saville

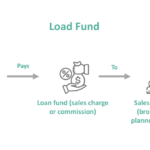

Paying a load is akin to throwing away most or all of the supposed advantage you get from having a salesman choose a fund for you. If it’s true that asset allocation accounts for 95 percent of investment results over long periods of time, then only 5 percent is left over as a reward for having the “right” fund and the “right” manager. But even if a salesman could help you pick that “right” fund, paying him a commission of 5 percent wipes out the benefit.

When you pay a 5 percent load you lose the opportunity to invest 5 percent of your money forever. When you buy a load fund, the money that goes to the salesman goes to work for him, not for you. When you invest in a no-load fund, all your money goes to work for you.

And load percentages are always higher than the quoted figures. For example in a $10,000 investment if $500 goes to the sales organization then $9,500 is invested on your behalf. Funds are allowed to call this a 5 percent commission. In fact, you invested only $9,500, and the $500 load amounts to a commission not of 5 percent but of 5.26 percent on your real investment.

Load amounts are higher than they look. The effect of your commission grows over time. If you avoided a $1,000 commission by investing in a no-load fund, over 25 years you would wind up with nearly $11,000 more if your money compounded at 10 percent. In other words, the $1,000 load would, in effect, be an $11,000 load.

The broker who chooses a fund for you may have a reason to prefer that you buy a poorer-performing fund instead of a top-performing one. Studies show that funds operated by brokerage houses (naturally, they are almost exclusively load funds) have poorer average performance than independent load funds. Yet a broker often earns exotic trips and other perks, in addition to a higher percentage of the commission, for selling house funds. So if you buy a load fund from a broker, at least insist on getting one that is not managed by that brokerage house. You’ll then get more objective guidance-and hopefully better performance.

On average, load funds charge higher expenses than no-load funds. These are the expenses that all funds take out of their assets, whether their investors pay loads or not. In a study that covered thousands of funds, Morningstar found that the average load fund charges its investors significantly more than the average no-load fund. Expense ratios among equity funds averaged 1.1 percent for no-loads and 1.6 percent for load funds. Among bond funds, the average was 0.6 percent for no-load funds and 1.1 percent for load funds. Those differences may seem small. But unlike a load, a fund’s expense charge hits you year after year after year. The longer you own a high-expense fund, the deeper it reaches into your pockets.

What should you do if you already have a load fund?

You shouldn�t necessarily sell that fund. The reasons for avoiding load funds cease to apply once you already own one. The reason is simple: Once you pay the load, your money is gone. Getting out of the fund won’t get it back. Therefore, if you are already in that position, there is no particular advantage to sell that fund just because of the load.

You shouldn�t necessarily keep the fund, either. If the fund has a back-end load, that provision may give you an incentive to leave your money in that fund. Sometimes, back-end loads are structured so that the longer you leave your money in the fund, the lower the load. You should study the prospectus to find this out, or have somebody help you with it. Or call the fund and ask about your options.

Don’t keep a fund just because of its back-end load. Even if you keep a back-end-load fund long enough to avoid most or all of the load, the salesperson still got paid the commission. The fund found some way to extract that money from you to cover its commission cost. This could account for some of the higher expenses that load funds levy on their shareholders. And, of course, you may be hit with annual 12b1 fees to cover marketing costs. If this is the case, then you may be paying those fees again and again, every year you own the fund.

In summary, the presence of a load is not reason enough to sell or keep a fund. The decision depends on the details of the load, your own circumstances and needs, and the quality of the fund itself.

Tinggalkan Balasan